A new blog by the CORPNET group had been published on Medium.com. The blog, “Neymar and State Money: How Sovereign Investment enters Global Capitalism”, is written by Milan Babic and Katie-Ann Wilson and can be found here.

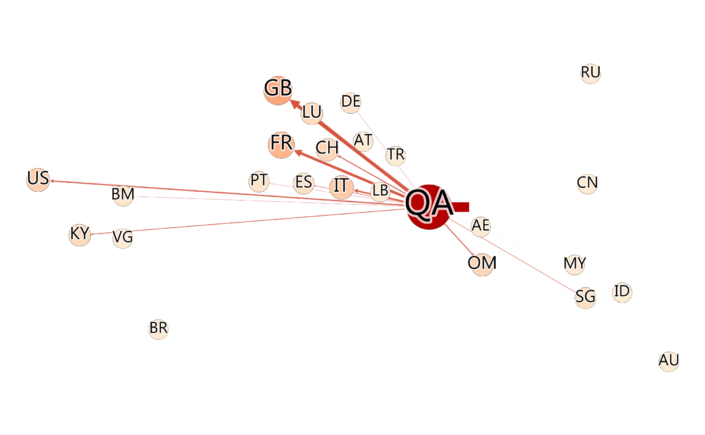

Abstract This blog post discusses the activities, outreach and role of the Qatar Investment Authority (QIA) that recently drew global attention by enabling the most expensive football player transfer in history. Besides the 222 Mio. € investment in Brazilian superstar Neymar, the QIA is very active as an investment fund around the world. The interesting and hardly studied aspect about the QIA is its status as wholly state-owned entity participating in global capitalism. CORPNET is able to track these activities on a global scale by looking at fine-grained ownership data. This investigation of cross-border state ownership networks goes beyond Sovereign Wealth Funds and can be extended to any state-owned entity around the world.

Public outcry over tax havens has increased in recent years. Journalists have shed light on the users of these offshore financial centres (OFCs), as well as the jurisdictions, banks, accountancy and law firms involved: OffshoreLeaks (2013), LuxLeaks (2014), SwissLeaks (2015), the Panama Papers (2015) and BahamasLeaks (2016).

OFCs are popular instruments for multinational corporations to (legally) reduce their tax bill by moving capital across borders in the form of dividends, royalties and interest by taking advantage of loopholes in the legislation. By playing out one state against another, corporations may reduce their tax rate from around 35% to 15-25% (and some much lower). For instance, Apple uses a combination of subsidiaries in Ireland, the Netherlands and Bermuda to strongly reduce its tax payments in Europe to a stunning 0.005% in 2014 according to the European Comission.

If profits would be accounted for where the economic activity takes place, multinationals would pay at least US$500-650 billion more on taxes, according to estimates by the Tax Justice Network and the International Monetary Fund. From this, around US$200 billion relates to developing countries, which means that developing countries lose more capital in tax avoidance than receive in development aid (US$142.6 billion).

What countries are Offshore Financial Centres?Given this contested role of OFCs it is surprising that we still lack a broadly accepted definition of what makes a country an OFC. Instead, the identification of OFC jurisdictions has become a politicised and contested issue. International organisations such as the OECD or the IMF have published lists of alleged tax havens (OECD list, IMF list), but the chosen criteria remained heavily influenced by politics.

To remedy this lack of transparency, we developed a novel, data-driven approach that identifies OFCs. We simply ask which countries or jurisdictions play a role in corporate ownership chains that is incommensurate with the size of their domestic economies (see Zoromé 2007). Our results show that offshore finance is not the exclusive business of exotic small islands far away. Countries such as the Netherlands and the United Kingdom play a crucial yet previously hidden role as conduits of offshore finance on its way to tax havens.

Using big data to find OFCs Early attempts at OFC identification have resulted in for instance the Tax Justice Network’s “Financial Secrecy Index” and Oxfam’s list of the worst corporate tax havens. Jan Fichtner’s “Offshore-intensity Ratio” provides a helpful rough yardstick to judge which jurisdictions act as OFCs by describing the proportion between foreign capital (such as FDI) and the size of the domestic economy. However, these measures do not allow us to differentiate if foreign investment reported by Bermuda originates in the Netherlands, or if in contrast it originates in Germany and is routed through the Netherlands. We still don’t know how offshore finance flows across the globe.

To overcome these problems we move from country level statistics to large scale company data. The coming together of political economists and computer scientists in the CORPNET research group at the University of Amsterdam made it possible to study how corporations make use of particular countries and jurisdictions in their international ownership structures.

We analyzed the entire global network of ownership relations, with information of over 98 million firms and 71 million ownership relations. Note that here we are interested in how OFCs cater to the needs of multinational corporations, and not private individuals. Unlike previous attempts at identifying OFCs, this granular firm-level network data allowed us to identify and distinguish what we call “sink-OFCs” and “conduit-OFCs.” With some surprising results.

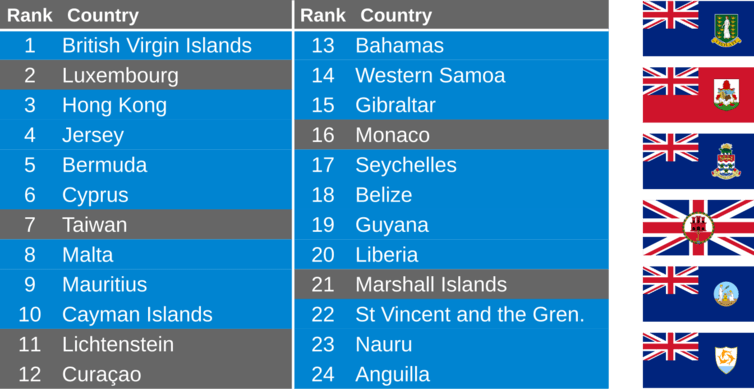

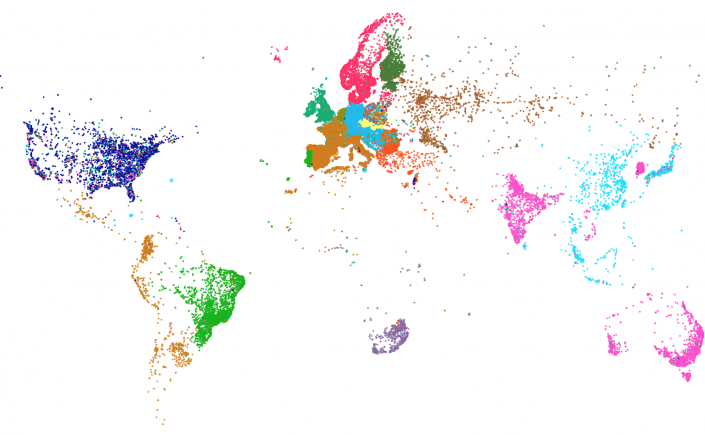

Introducing sinks and conduits Sink-OFCs attract and retain foreign capital. Our approach identifies 24 sink-OFCs, including Luxembourg, Hong Kong, the

Figure: Sink Offshore Financial Centers (jurisdictions in blue have been under British sovereignty in the past or are still UK dependencies

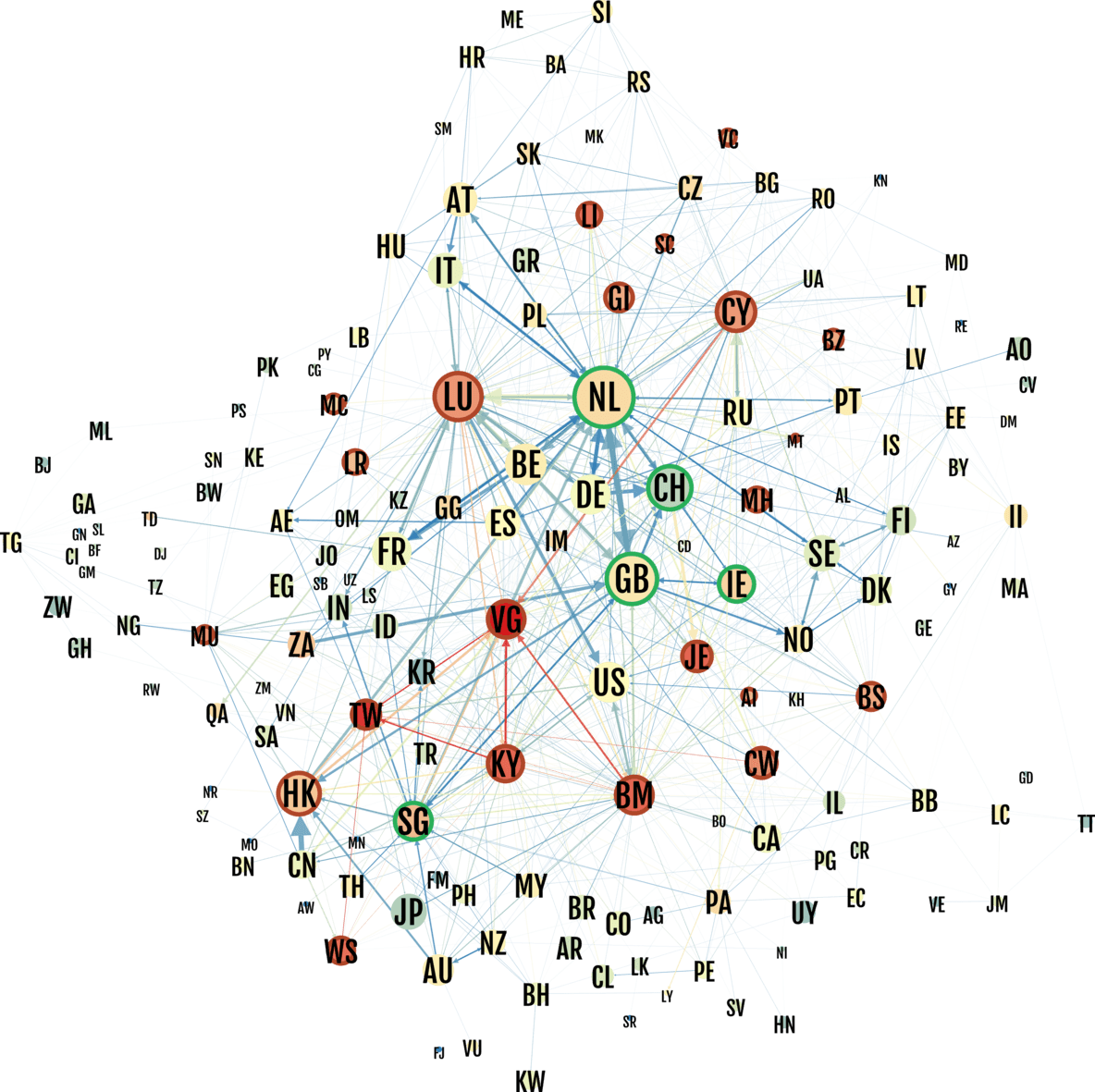

Using our method we can now also investigate which jurisdictions are used by corporations en route to sinks. These conduit-OFCs are attractive intermediate destinations and enable the transfer of capital without taxation.

Surprisingly we found that only five big countries act as conduit-OFCs. Together these five conduits funnel 47% of corporate offshore investment from tax havens, according to the data we analysed. The two largest conduits by far are the Netherlands (23%) and the United Kingdom (14%). They are followed by Switzerland (6%), Singapore (2%) and Ireland (1%).

Figure: Network of relationships between countries. Conduits are marked in green, sinks are marked in red. The size of the country is proportional to the investment flows through the country and the colour to its position as a sink (blue = no sink, red = sink). The size of the arrows is proportional to the investment between two countries and the colour to its importance (blue = lower flow than expected, red = higher flow than expected).

Figure: Network of relationships between countries. Conduits are marked in green, sinks are marked in red. The size of the country is proportional to the investment flows through the country and the colour to its position as a sink (blue = no sink, red = sink). The size of the arrows is proportional to the investment between two countries and the colour to its importance (blue = lower flow than expected, red = higher flow than expected).

Conclusion

Offshore Financial Centers are often portrayed as small, exotic, far away islands that are difficult if not impossible to regulate. We show that many OFCs are in fact highly developed countries.

Since the financial crisis, the EU and the OECD have increased pressure on tax avoidance, with modest effects. We hope that our approach can help regulators target the policy to the sectors and territories where the offshore activity concentrates. In particular, targeting conduit-OFCs could prove more effective than targeting sink-OFCs, since – while new territories with low or no corporate taxes are continuously emerging – the conditions for conduit-OFCs (numerous tax treaties, strong legal systems, good reputation) can only be found in a few countries.

Results and details are available on the dedicated website www.uva.nl

A new article by the CORPNET group has been published in the June 2017 issue of the Antitrust Chronicle (pp. 51-57). The piece, “The New Mandate Owners: Passive Asset Managers and the Decoupling of Corporate Ownership”, is written by Carmel Shenkar, Eelke Heemskerk and Jan Fichtner and can be found here.

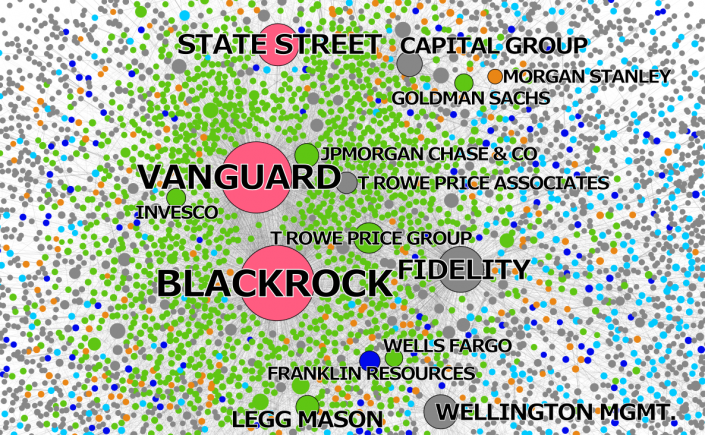

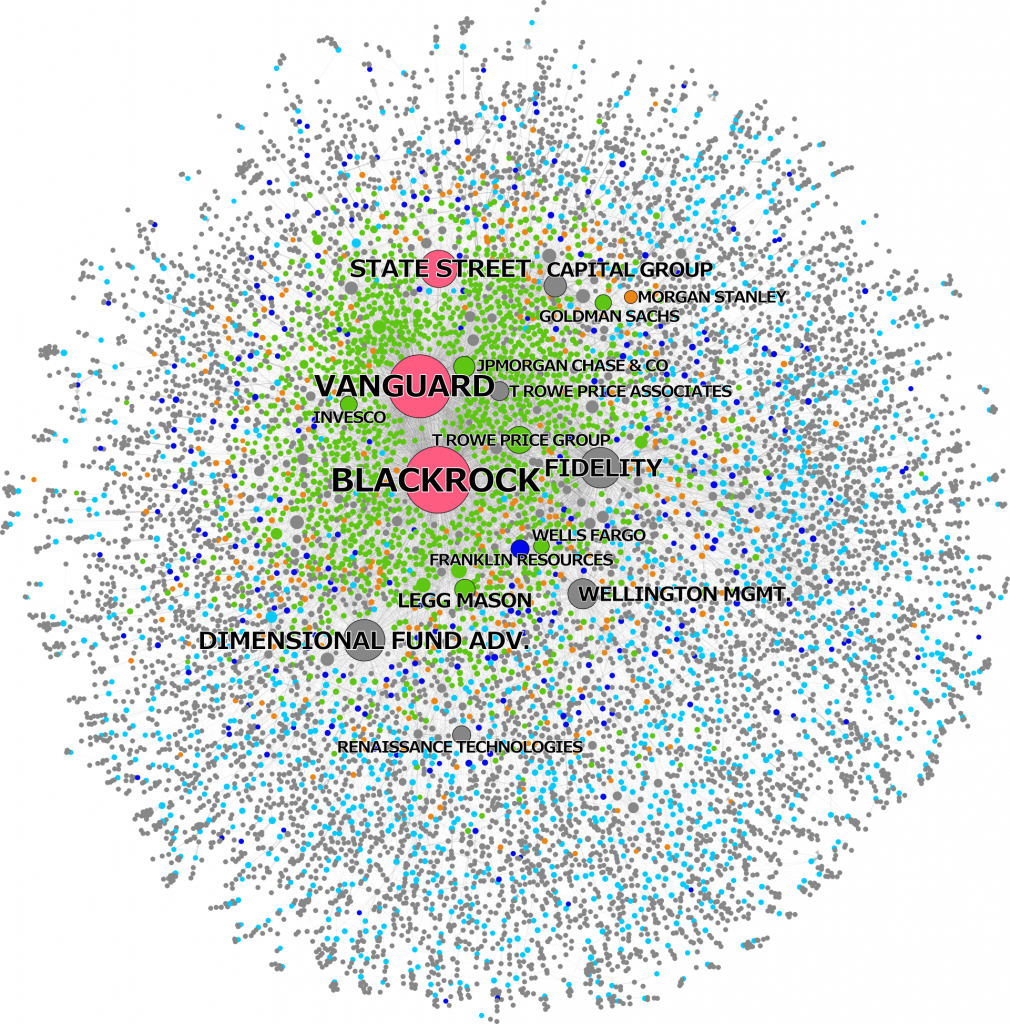

Abstract A major shift toward passively managed index funds in recent years has led to the re-concentration of corporate ownership in the hands of just three large asset management firms, the Big Three: BlackRock, Vanguard and State Street. We propose that this trend has re-structured ownership in capital markets. Adopting a contractual view to the corporate share, we re-define share holding and suggest that the New Mandate Owners in fact hold the essence of corporate power, as their aggregated positions capture the core element of the franchise of corporate voting.

A new paper by the CORPNET group has been published in the June issue of Business and Politics journal (pp: 298-326). The article, “Hidden power of the Big Three? Passive index funds, re-concentration of corporate ownership, and new financial risk”, is written by Jan Fichtner, Eelke Heemskerk and Javier Garcia-Bernardo and can be found here.

Abstract Since 2008, a massive shift has occurred from active toward passive investment strategies. The passive index fund industry is dominated by BlackRock, Vanguard, and State Street, which we call the “Big Three.” We comprehensively map the ownership of the Big Three in the United States and find that together they constitute the largest shareholder in 88 percent of the S&P 500 firms. In contrast to active funds, the Big Three hold relatively illiquid and permanent ownership positions. This has led to opposing views on incentives and possibilities to actively exert shareholder power. Some argue passive investors have little shareholder power because they cannot “exit,” while others point out this gives them stronger incentives to actively influence corporations. Through an analysis of proxy vote records we find that the Big Three do utilize coordinated voting strategies and hence follow a centralized corporate governance strategy. However, they generally vote with management, except at director (re-)elections. Moreover, the Big Three may exert “hidden power” through two channels: First, via private engagements with management of invested companies; and second, because company executives could be prone to internalizing the objectives of the Big Three. We discuss how this development entails new forms of financial risk.

CORPNET receives an NWO Visitors Grant to host dr. Michał Zdziarski, Head of Strategic Management and International Business at University of Warsaw. With the NWO Visitors grant researchers can host highly qualified senior researchers from abroad for a maximum of four months.

Michał Zdziarski is currently working with the CORPNET group on the global topology of business groups. The research interest in particular is to better understand social distance as driver for firm strategic behavior, such as foreign market entry.

A new article by the CORPNET group has been published in issue 2 of 2016 of the sociologica journal. The piece, ‘Where is the global corporate elite? A large-scale network study of local and nonlocal interlocking directorates‘, is written by Eelke Heemskerk, Frank Takes, Javier Garcia-Bernardo and Jouke Huijzer and can be found here.

Abstract Business élites reconfigure their locus of organization over time, from the city level, to the national level, and beyond. We ask what the current level of élite organization is and propose a novel theoretical and empirical approach to answer this question. Building on the universal distinction between local and nonlocal ties we use network analysis and community detection to dissect the global network of interlocking directorates among over five million firms. We find that élite orientation is indeed changing from the national to the transnational plane, but we register a considerable heterogeneity across different regions in the world. In some regions the business communities are organized along national borders, whereas in other areas the locus of organization is at the city level or international level. London dominates the global corporate élite network. Our findings underscore that the study of corporate élites requires an approach that is sensitive to levels of organization that go beyond the confines of nation states.

A blog by the CORPNET group can be found on the LSE Business Review website. The piece, ‘Network analysis shows offshore finance as a complex network of ownership ties’, is written by Jan Fichtner and can be found here.

Abstract

The EU made a move in August to force Apple to pay €13 billion in unpaid taxes. The episode has quickly become emblematic of the EU’s fight against corporate tax avoidance, a dispute which intensified in the aftermath of the 2009 financial crisis. As Europeans see it, this is about the need to provide a level playing field between US and EU businesses. If a UK-based retailer pays a lot more taxes than US-based Amazon, it will never be able to compete fairly. The OECD, “the organisation charged by the G8 and more recently the G20 to develop international standards as part of the fight against tax avoidance and evasion” saw its ambitions watered down after intense political pressure. In this article, CORPNET’s network analysis allows us to visualise how multinational corporations structure their ownership ties, a key element in tax avoidance.

This blog post discusses existing research on the still rather opaque topic of offshore finance. Subsequently, it is outlined how the CORPNET team is going to shed some new light on this crucial topic by analyzing transnational ownership ties of multinational corporations utilizing complex networks methods and the ‘big data’ provided by the Orbis database.

Offshore finance is no longer the small and peripheral phenomenon it once was. During the last four decades, offshore finance has become a crucial element of the contemporary international political economy. Today, offshore financial centers (which can also be called tax havens or regulatory havens) constitute central nodes within global financial markets. Gabriel Zucman has recently estimated that financial wealth to the tune of almost US$8 trillion is held offshore – a sum that amounts to almost 50% of the GDP of the EU or the US. This causes a global tax revenue loss of approximately US$200 billion. Estimates for offshore wealth by the Tax Justice Network even range between US$21 and US$32 trillion. Arguably, high-net-worth individuals (HNWIs) and big multinational corporations (MNCs) hold the vast majority of this offshore wealth, which leads directly to questions of increasing economic inequality.

The impact of offshore finance not only pertains to economic inequality but also to questions of corporate accountability and transparency – both of which are pivotal to the proper functioning of any market economy. For this reason, the Tax Justice Network does not use the term offshore financial centers or tax havens, but instead calls them secrecy jurisdictions, because secrecy and opacity are major reasons why foreign economic actors use these countries and territories. With this secrecy and lack of accountability come big risks. The corporate scandals of Enron, Olympus and Parmalat as well as the near-collapse of the large hedge fund LTCM all involved subsidiaries in tax havens. In addition, these secrecy jurisdictions have functioned as legal domiciles for the creation of complex structured financial products, such as collateralized debt obligations (CDOs) and other asset-backed securities (ABSs). According to Photis Lysandrou and Anastasia Nesvetailova, these opaque financial products have contributed to the development of the global financial crisis, or at least have aggravated it significantly.

Despite these significant risks, offshore finance receives too little attention from regulators. Granted, the G20 have taken some (modest) measures after the global financial crisis to increase the regulation of offshore financial centers but Niels Johannesen and Gabriel Zucman have found that these measures have only caused a relocation of assets between offshore centers, but not a general decline of assets booked in these secrecy jurisdictions.

But the heat is on. In 2014, the International Consortium of Investigative Journalists (ICIJ) published a report that gained worldwide media attention: the “Luxembourg Leaks.” The ICIJ report revealed that the Grand Duchy of Luxembourg helped over 300 large multinational corporations to lower their global tax bills drastically, Amazon, McDonalds and IKEA for example. These big companies have channeled hundreds of billions of dollars through this tiny jurisdiction and as a result saved billions of dollars in taxes elsewhere. Another example, which has drawn a lot of attention is a tax construction known as the “Double Irish With a Dutch Sandwich” that reduces taxes for large multinationals, such as Apple, by shifting international profits from an Irish subsidiary to the Netherlands then back to Ireland and subsequently elsewhere, e.g. to Caribbean tax havens. In mid-2016, the European Union has ruled that the special tax construction that Ireland has offered Apple constitutes an illegal and unfair subsidy amounting to over US$13 billion, which has to be repaid. Finally, the massive leak of confidential data concerning letterbox companies and trusts known as the “Panama Papers” that included data on over 200,000 offshore entities caused widespread attention by the media and by academia alike.

Identifying Offshore Financial Centers

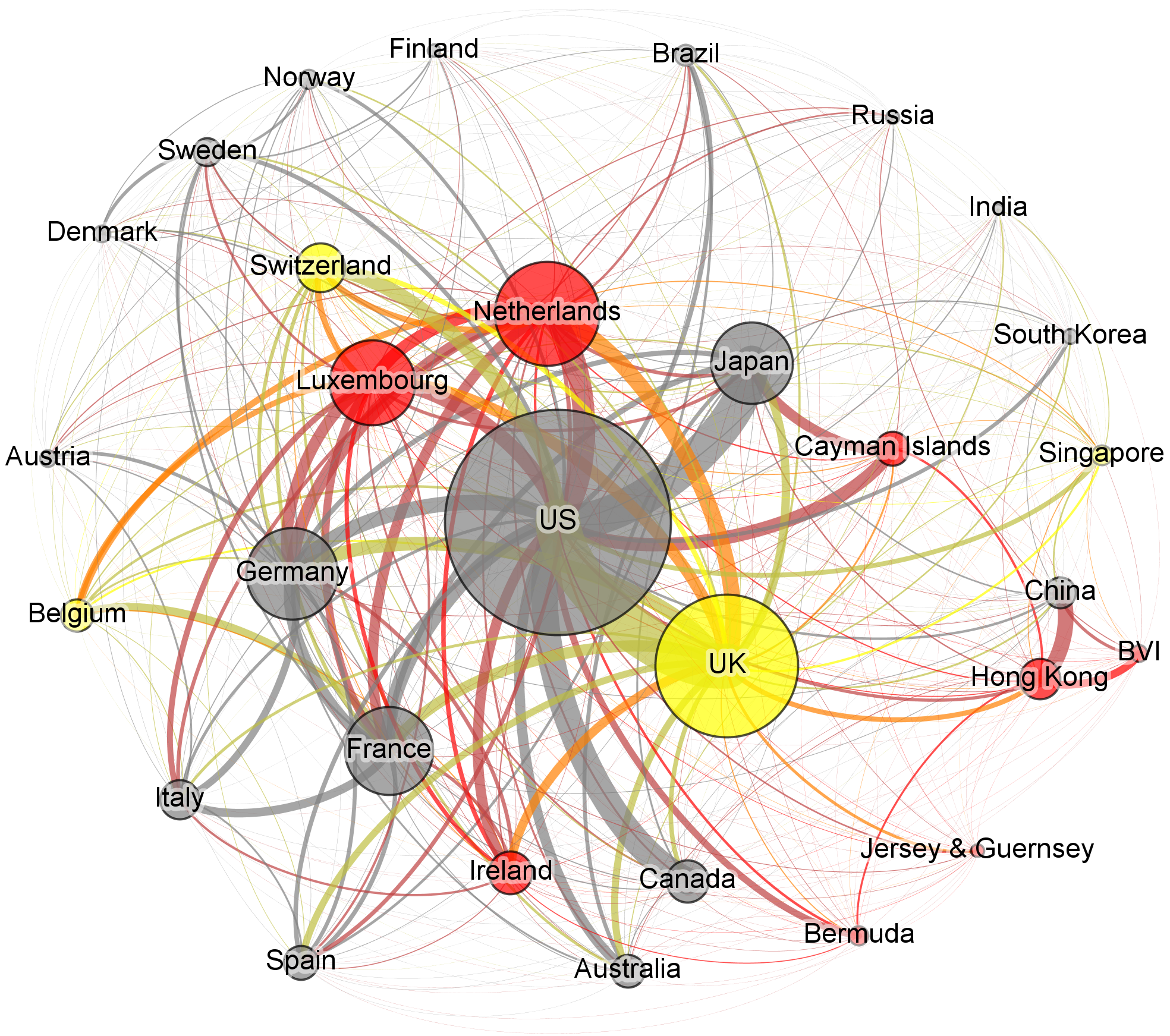

A number of international organizations, such as the IMF, the OECD and others, started to publish lists of countries deemed to be offshore centers. Of course, such lists – even if initially based on relevant criteria – quickly become politicized and therefore often lose their value. One definition of offshore financial centers that is well suited for empirical research is from Ahmed Zoromé: “an OFC is a country or jurisdiction that provides financial services to nonresidents on a scale that is incommensurate with the size and the financing of its domestic economy.” This definition has the advantage that it is exclusively based on data. The Financial Secrecy Index as well the Offshore-Intensity Ratio follow this methodological approach. The Financial Secrecy Index combines a secrecy score with a global scale weight to produce a FSI–Value for each jurisdiction. The Offshore-Intensity Ratio sets the aggregated amount of foreign capital booked in a jurisdiction (external bank deposits, foreign portfolio investment, and foreign direct investment) in relation to the size of its domestic economy. The result is a ratio that expresses the strength with which the particular jurisdiction has acted as a magnet for foreign capital. Figure 1 shows the bilateral financial relations between the largest 34 jurisdictions of cross-border global finance. These transnational financial ties amount to almost US$82 trillion – slightly more than global GDP. You can read the figure as follows: grey are the countries least likely to be an offshore financial center. Yellow are potential OFCs, such as Switzerland and the UK. Finally, the red countries have high Offshore-Intensity Ratios, including Ireland, Luxembourg and the Netherlands. The magnitude of the spheres in the visualization is equivalent to the sum of all their bilateral relations in the field of cross-border global finance. The largest jurisdictions are at the center of the visualization, the smaller ones are shown at the periphery.

Both the Financial Secrecy Index as well as the Offshore-Intensity Ratio are based on aggregated data, i.e. combining all foreign portfolio or direct investment that has been reported to international organizations. In fact, aggregated data are used by the vast majority of existing studies on offshore financial centers. However, it is in the very nature of aggregated data that many interesting and relevant details are conflated. This precludes the application of many innovative research questions and methods. Therefore, a promising approach to the analysis of offshore finance is to use disaggregated, granular data. The CORPNET research group uses the Orbis database by Bureau van Dijk, which contains 200 million firms, 70 million corporate ownership relationships, and 10 million transnational ownership chains. Granular, firm-based data allow us to study new research questions concerning offshore financial centers and how they are used by multinational corporations to minimize (and most likely also evade) taxes and to create secret and opaque transnational corporate ownership structures (see this paper by Alex Cobham and Simon Loretz for innovative research using Orbis data).

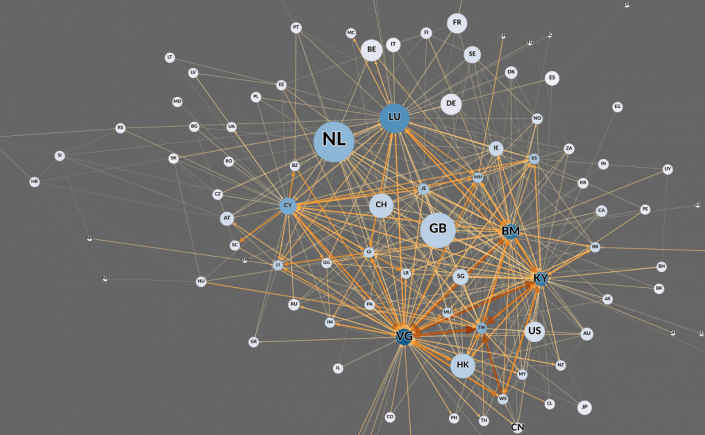

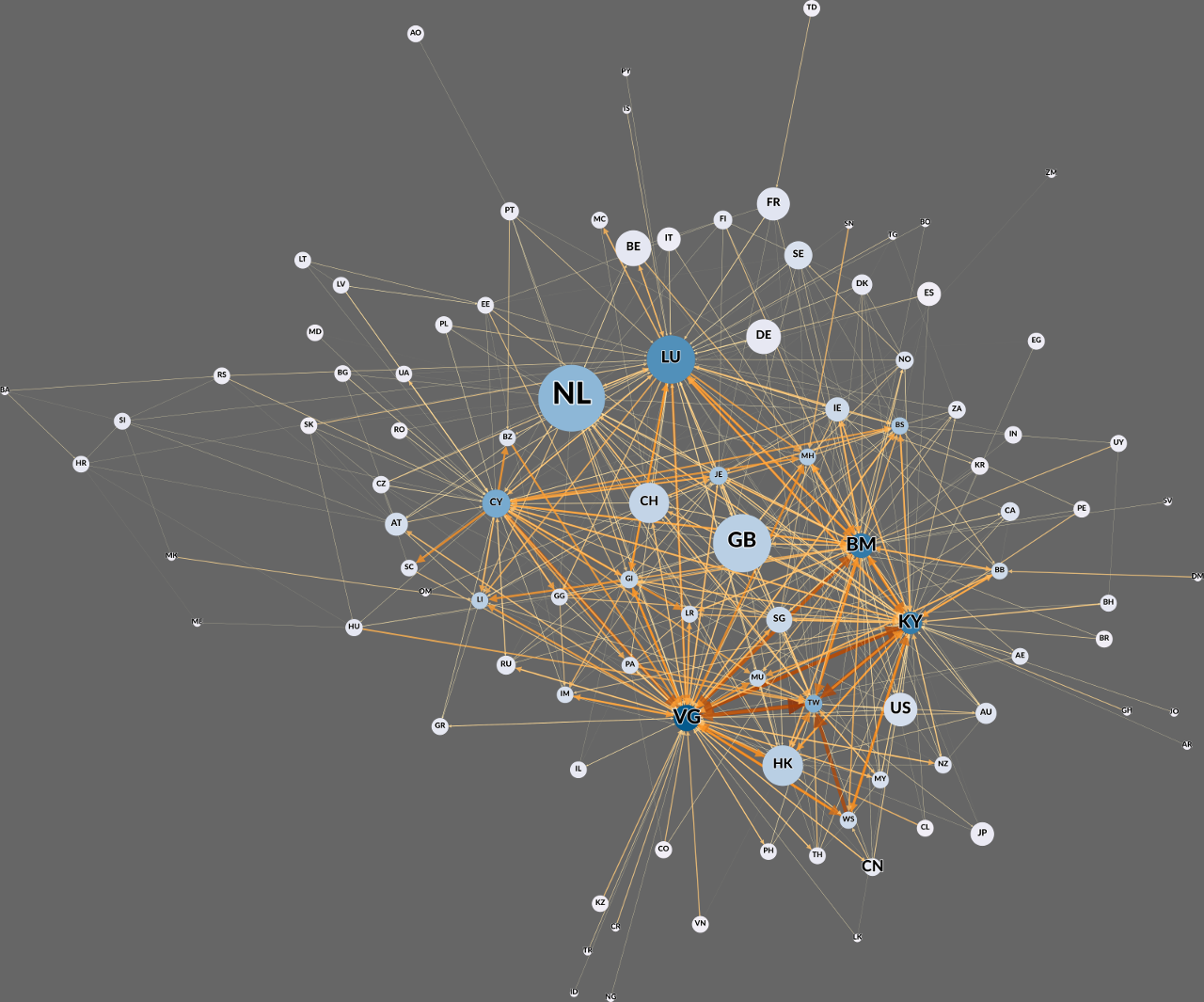

In the next step, CORPNET is going to focus on what we call “Global Ownership Chains” (GOCs), which are corporate ownership relations (often via subsidiaries) that span across multiple jurisdictions, presumably in order to minimize and evade taxes, and to create secrecy and opacity. Here, we are inspired by and build upon research on “Global Value Chains” and “Global Wealth Chains”. Existing research on corporate ownership chains is scant. The United Nations Conference on Trade and Development (UNCTAD) has published some groundbreaking research on ownership chains in its 2016 World Investment Report, inter alia introducing an “investor nationality mismatch index” (also relying on Orbis data). We are going to complement and expand this emerging literature by identifying the (offshore) jurisdictions that play the most important role in GOCs. Preliminary results indicate that only a small number of jurisdictions dominate GOCs – primarily the Netherlands, but also Luxembourg, the United Kingdom, Bermuda (BM), the Cayman Islands (KY), and the British Virgin Islands (VG) (see Figure 2). Thus, CORPNET is going to advance the research on offshore finance by analyzing it as a complex network of transnational ownership ties.

Figure 2: The Network of Transnational Ownership Ties by Value Going Through Chains in 2015.

Source: CORPNET analysis by Javier Garcia-Bernardo based on Orbis data.

Interested in learning more about the CORPNET group? Do feel free to contact us

This blog post was written by Jan Fichtner, postdoctoral researcher in the CORPNET group at the University of Amsterdam.

Since 2008, a massive shift has occurred from active towards passive investment strategies. This burgeoning passive index fund industry is dominated by BlackRock, Vanguard, and State Street, which we call the ‘Big Three’. In a new working paper CORPNET shows that already in 40 percent of all listed U.S. corporations the Big Three together constitute the largest shareholder — and even in 88 percent of the S&P 500 firms. This re-concentration of ownership is unprecedented and unlike the earlier ascent of actively managed mutual funds, such as Fidelity, is likely here to stay.

In contrast to active funds, the Big Three hold illiquid and permanent ownership positions, which give them stronger incentives to actively influence corporations. An analysis of the voting records on shareholder meetings reveals that the Big Three indeed utilize coordinated voting strategies but generally vote with management, except at director (re-)elections. Private engagements with management represent an important channel through which the Big Three exert influence.

Moreover, BlackRock, Vanguard, and State Street are arguably exerting ‘hidden power’ because company executives are likely to internalize their objectives. Finally, we find indications that this development entails new forms of financial risk, including anticompetitive effects and investor herding.