On the 4th of December “The Spider’s Web – An investigation into the world of Britain’s secrecy jurisdictions and the City of London” will be screened at CREA Amsterdam.

States lose 600 billion dollars in taxes through corporate tax avoidance practices spanning several countries. Some of these countries, such as the United Kingdom or the Netherlands play a key role facilitating tax avoidance, as recent studies by researchers at the University of Amsterdam showed.

The Spider’s Web is a documentary film that shows how Britain transformed from a colonial power into a global financial power. At the demise of empire, the City of London created a web of offshore secrecy jurisdictions that captured wealth from across the globe and hid it behind obscure financial structures. Today, up to half of global offshore wealth is estimated to be hidden in British offshore jurisdictions and Britain and its offshore jurisdictions are the largest global players in the world of international finance. How did this come about, and what impact does it have on the world today? This is what the Spider’s Web sets out to investigate.

After the film, the public will get the opportunity to address questions directly to the filmmakers in London and an expert panel. Subsequently, we will discuss the role of the Netherlands in offshore finance, and the advantages and drawbacks for Dutch and European citizens.

Panel participants:

Rodrigo Fernandez, expert on tax avoidance from SOMO

Ewald Engelen, prof. of Financial Geography at the UvA

John Christensen, director of the Tax Justice Network

Moderation: Eelke Heemskerk, program director of the CORPNET research team

CREA Amsterdam

Nieuwe Achtergracht 170, 1018WV Amsterdam

Monday December 4th 20:00- 23.59

A new blog by the CORPNET group has been published by the LSE Latin America and Caribbean Centre. The blog, “The Cayman conundrum: why is one tiny archipelago the largest financial centre in Latin America and the Caribbean?”, is written by Jan Fichtner and can be found here.

Abstract Analysinghow millions of multinational corporations structure their global ownerships chains reveals that Cayman acts as a ‘sink’ offshore financial centre where foreign capital accumulates and data trails often end, writes Jan Fichtner (University of Amersterdam).

A new paper by the CORPNET group has been published in the Global Networks journal. The article, “When theory meets methods: the naissance of computer assisted corporate interlock research”, is written by Meindert Fennema and Eelke Heemskerk and can be found here.

Abstract In this article, we study the emergence of computer aided network analysis as an example of ‘Mertonian’ multiple discovery. Computer assisted quantitative network analysis emerged around 1970 and small groups of researchers in different universities, who were independent of each other and looking for the right concepts and computer programs to implement graph theory in social analysis, first applied it to corporate interlock networks. We show how mathematical graph theory provided a toolbox for systematic network analysis and that simultaneously in the Netherlands and the United States this toolbox found an application in the study of corporate power. A historical narrative covers the three main centres in which large-scale corporate network analysis emerged – Amsterdam, California and Stony Brook. For each centre, we provide a sketch of the people involved, the tools they used, and the motivations that brought them to this topic. Our analysis makes clear that one cannot understand the emergence of computer aided network analysis without considering the personal and often political motivations of those who engaged in the first board interlock studies. Insurgent students of political science and sociology pushed for a research agenda on corporate power and found support from scholars who were keen to develop innovative network analysis methods. Hence, corporate network analysis became a legitimate field of research.

A member of the CORPNET group, Frank Takes, has won the Young eScientist Award 2017. The prize aims to stimulate a young scientist demonstrating excellence in eScience: the development or application of digital technology to address scientific challenges. The prize will be used to undertake a joint research project, in which Takes will receive support by eScience Research Engineers (experts in the development and application of research software). More information can be found here.

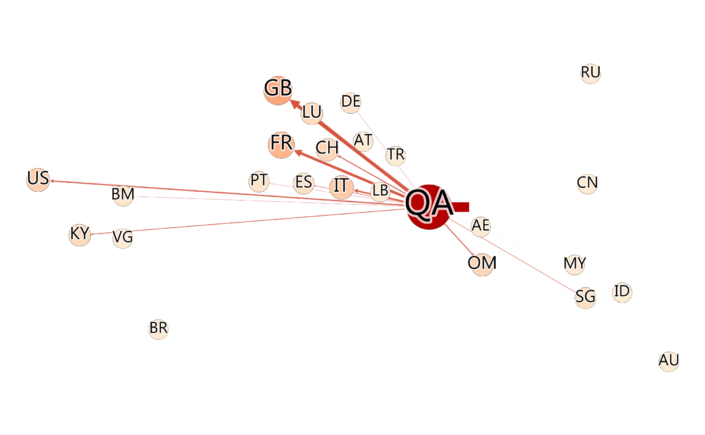

A new blog by the CORPNET group had been published on Medium.com. The blog, “Neymar and State Money: How Sovereign Investment enters Global Capitalism”, is written by Milan Babic and Katie-Ann Wilson and can be found here.

Abstract This blog post discusses the activities, outreach and role of the Qatar Investment Authority (QIA) that recently drew global attention by enabling the most expensive football player transfer in history. Besides the 222 Mio. € investment in Brazilian superstar Neymar, the QIA is very active as an investment fund around the world. The interesting and hardly studied aspect about the QIA is its status as wholly state-owned entity participating in global capitalism. CORPNET is able to track these activities on a global scale by looking at fine-grained ownership data. This investigation of cross-border state ownership networks goes beyond Sovereign Wealth Funds and can be extended to any state-owned entity around the world.

Public outcry over tax havens has increased in recent years. Journalists have shed light on the users of these offshore financial centres (OFCs), as well as the jurisdictions, banks, accountancy and law firms involved: OffshoreLeaks (2013), LuxLeaks (2014), SwissLeaks (2015), the Panama Papers (2015) and BahamasLeaks (2016).

OFCs are popular instruments for multinational corporations to (legally) reduce their tax bill by moving capital across borders in the form of dividends, royalties and interest by taking advantage of loopholes in the legislation. By playing out one state against another, corporations may reduce their tax rate from around 35% to 15-25% (and some much lower). For instance, Apple uses a combination of subsidiaries in Ireland, the Netherlands and Bermuda to strongly reduce its tax payments in Europe to a stunning 0.005% in 2014 according to the European Comission.

If profits would be accounted for where the economic activity takes place, multinationals would pay at least US$500-650 billion more on taxes, according to estimates by the Tax Justice Network and the International Monetary Fund. From this, around US$200 billion relates to developing countries, which means that developing countries lose more capital in tax avoidance than receive in development aid (US$142.6 billion).

What countries are Offshore Financial Centres?Given this contested role of OFCs it is surprising that we still lack a broadly accepted definition of what makes a country an OFC. Instead, the identification of OFC jurisdictions has become a politicised and contested issue. International organisations such as the OECD or the IMF have published lists of alleged tax havens (OECD list, IMF list), but the chosen criteria remained heavily influenced by politics.

To remedy this lack of transparency, we developed a novel, data-driven approach that identifies OFCs. We simply ask which countries or jurisdictions play a role in corporate ownership chains that is incommensurate with the size of their domestic economies (see Zoromé 2007). Our results show that offshore finance is not the exclusive business of exotic small islands far away. Countries such as the Netherlands and the United Kingdom play a crucial yet previously hidden role as conduits of offshore finance on its way to tax havens.

Using big data to find OFCs Early attempts at OFC identification have resulted in for instance the Tax Justice Network’s “Financial Secrecy Index” and Oxfam’s list of the worst corporate tax havens. Jan Fichtner’s “Offshore-intensity Ratio” provides a helpful rough yardstick to judge which jurisdictions act as OFCs by describing the proportion between foreign capital (such as FDI) and the size of the domestic economy. However, these measures do not allow us to differentiate if foreign investment reported by Bermuda originates in the Netherlands, or if in contrast it originates in Germany and is routed through the Netherlands. We still don’t know how offshore finance flows across the globe.

To overcome these problems we move from country level statistics to large scale company data. The coming together of political economists and computer scientists in the CORPNET research group at the University of Amsterdam made it possible to study how corporations make use of particular countries and jurisdictions in their international ownership structures.

We analyzed the entire global network of ownership relations, with information of over 98 million firms and 71 million ownership relations. Note that here we are interested in how OFCs cater to the needs of multinational corporations, and not private individuals. Unlike previous attempts at identifying OFCs, this granular firm-level network data allowed us to identify and distinguish what we call “sink-OFCs” and “conduit-OFCs.” With some surprising results.

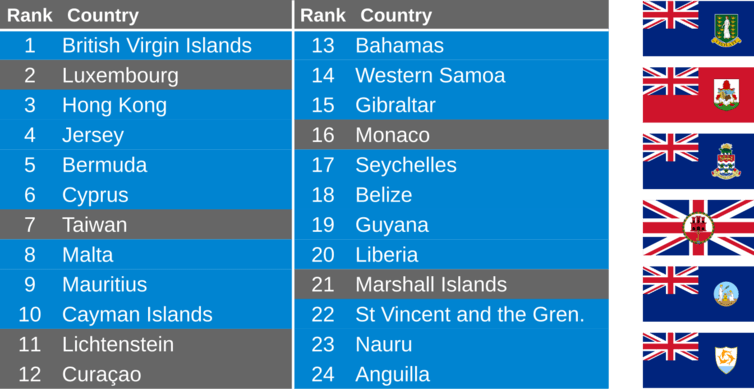

Introducing sinks and conduits Sink-OFCs attract and retain foreign capital. Our approach identifies 24 sink-OFCs, including Luxembourg, Hong Kong, the

Figure: Sink Offshore Financial Centers (jurisdictions in blue have been under British sovereignty in the past or are still UK dependencies

Using our method we can now also investigate which jurisdictions are used by corporations en route to sinks. These conduit-OFCs are attractive intermediate destinations and enable the transfer of capital without taxation.

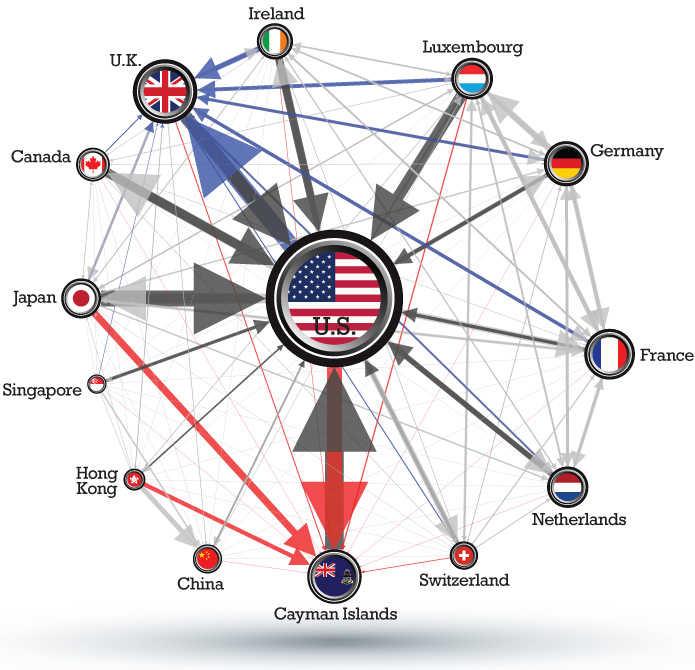

Surprisingly we found that only five big countries act as conduit-OFCs. Together these five conduits funnel 47% of corporate offshore investment from tax havens, according to the data we analysed. The two largest conduits by far are the Netherlands (23%) and the United Kingdom (14%). They are followed by Switzerland (6%), Singapore (2%) and Ireland (1%).

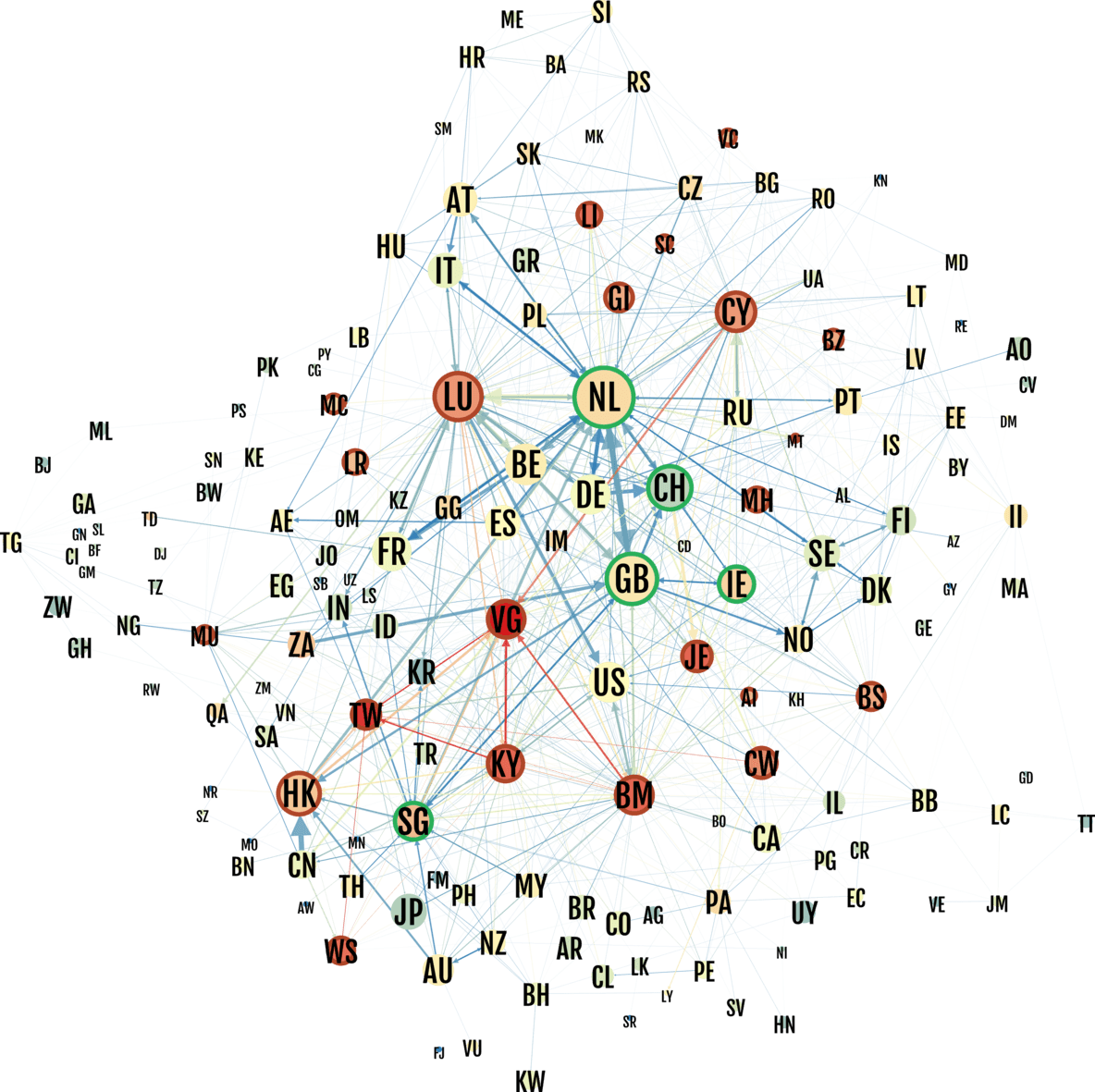

Figure: Network of relationships between countries. Conduits are marked in green, sinks are marked in red. The size of the country is proportional to the investment flows through the country and the colour to its position as a sink (blue = no sink, red = sink). The size of the arrows is proportional to the investment between two countries and the colour to its importance (blue = lower flow than expected, red = higher flow than expected).

Figure: Network of relationships between countries. Conduits are marked in green, sinks are marked in red. The size of the country is proportional to the investment flows through the country and the colour to its position as a sink (blue = no sink, red = sink). The size of the arrows is proportional to the investment between two countries and the colour to its importance (blue = lower flow than expected, red = higher flow than expected).

Conclusion

Offshore Financial Centers are often portrayed as small, exotic, far away islands that are difficult if not impossible to regulate. We show that many OFCs are in fact highly developed countries.

Since the financial crisis, the EU and the OECD have increased pressure on tax avoidance, with modest effects. We hope that our approach can help regulators target the policy to the sectors and territories where the offshore activity concentrates. In particular, targeting conduit-OFCs could prove more effective than targeting sink-OFCs, since – while new territories with low or no corporate taxes are continuously emerging – the conditions for conduit-OFCs (numerous tax treaties, strong legal systems, good reputation) can only be found in a few countries.

Results and details are available on the dedicated website www.uva.nl

A new article by the CORPNET group has been published in the June 2017 issue of the Antitrust Chronicle (pp. 51-57). The piece, “The New Mandate Owners: Passive Asset Managers and the Decoupling of Corporate Ownership”, is written by Carmel Shenkar, Eelke Heemskerk and Jan Fichtner and can be found here.

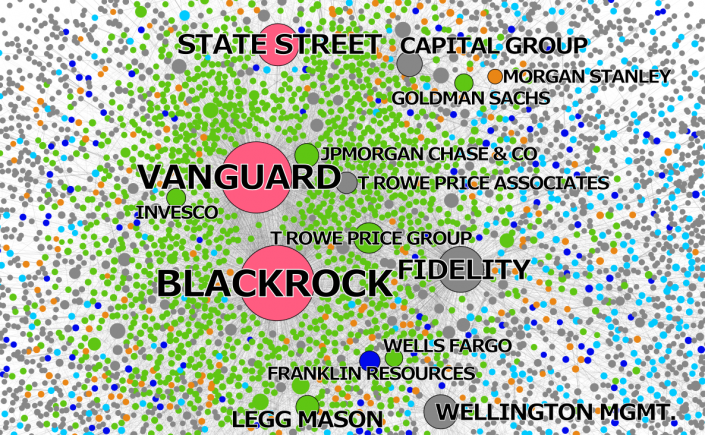

Abstract A major shift toward passively managed index funds in recent years has led to the re-concentration of corporate ownership in the hands of just three large asset management firms, the Big Three: BlackRock, Vanguard and State Street. We propose that this trend has re-structured ownership in capital markets. Adopting a contractual view to the corporate share, we re-define share holding and suggest that the New Mandate Owners in fact hold the essence of corporate power, as their aggregated positions capture the core element of the franchise of corporate voting.

A new paper by the CORPNET group has been published in the June issue of Business and Politics journal (pp: 298-326). The article, “Hidden power of the Big Three? Passive index funds, re-concentration of corporate ownership, and new financial risk”, is written by Jan Fichtner, Eelke Heemskerk and Javier Garcia-Bernardo and can be found here.

Abstract Since 2008, a massive shift has occurred from active toward passive investment strategies. The passive index fund industry is dominated by BlackRock, Vanguard, and State Street, which we call the “Big Three.” We comprehensively map the ownership of the Big Three in the United States and find that together they constitute the largest shareholder in 88 percent of the S&P 500 firms. In contrast to active funds, the Big Three hold relatively illiquid and permanent ownership positions. This has led to opposing views on incentives and possibilities to actively exert shareholder power. Some argue passive investors have little shareholder power because they cannot “exit,” while others point out this gives them stronger incentives to actively influence corporations. Through an analysis of proxy vote records we find that the Big Three do utilize coordinated voting strategies and hence follow a centralized corporate governance strategy. However, they generally vote with management, except at director (re-)elections. Moreover, the Big Three may exert “hidden power” through two channels: First, via private engagements with management of invested companies; and second, because company executives could be prone to internalizing the objectives of the Big Three. We discuss how this development entails new forms of financial risk.

CORPNET receives an NWO Visitors Grant to host dr. Michał Zdziarski, Head of Strategic Management and International Business at University of Warsaw. With the NWO Visitors grant researchers can host highly qualified senior researchers from abroad for a maximum of four months.

Michał Zdziarski is currently working with the CORPNET group on the global topology of business groups. The research interest in particular is to better understand social distance as driver for firm strategic behavior, such as foreign market entry.